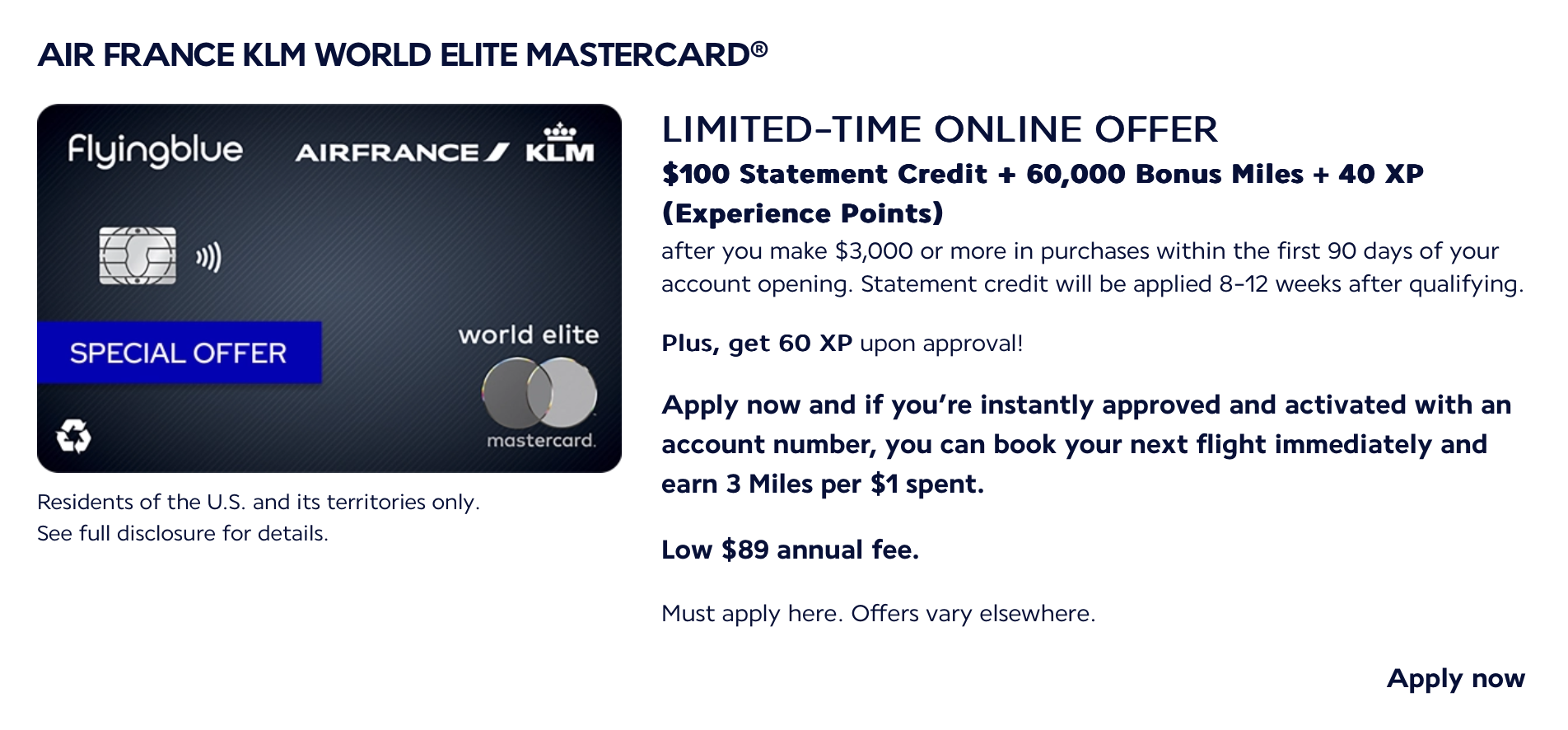

- Yesterday’s post mentioned in fake-shakespeare obtuseness that Rapid Rewards points value shifts based on demand; based on questions and comments I got yesterday, that wasn’t clear to many. To speak in ye-new-modern-day-English: Southwest Rapid Rewards points will no longer have a fixed redemption value for each class of ticket, but rather the redemption value will vary based on demand.

In other words, Rapid Rewards which already had dynamic pricing based on ticket value, will now have a dynamic redemption value per point too. To quote the quiet grandmaster churner RabbMD, “double secret dynamic” pricing. - Harris Teeter stores have a coupon for fee-free variable load Mastercard and Visa gift cards when loaded with $150+ through Tuesday, limit one per Kroger account. (Thanks to GCA)

- Rakuten’s In-Store card linked program has offers for several grocery stores:

– 1% or 1x at Giant

– 1% or 1x at Giant Food (different than the above, duh)

– 1% or 1x at Martins

– 1% or 1x at Food Lion

These are valid for 75 days after clipping the coupon. But after first use, the coupon is only valid for another hour, at which point you can reclip it as long as the promotion is still going. Why so complex? Well, remember that Rakuten is the company that bought Buy.com for $250 Million and decided that Buy.com was too hard for Americans to pronounce and remember, so just migrated it to Rakuten.com. - Some discount airlines, sorted in order of recent annoyingness, are running promotions:

– Breeze 50% off: Book by today, fly between March 18 and June 18 with promo GROW

– Frontier award sale: Book by Monday, fly through August 18

– Alaska international sale*: Book by April 11, fly through July 31

– [this space left intentionally blank]

– [this space left intentionally blank]

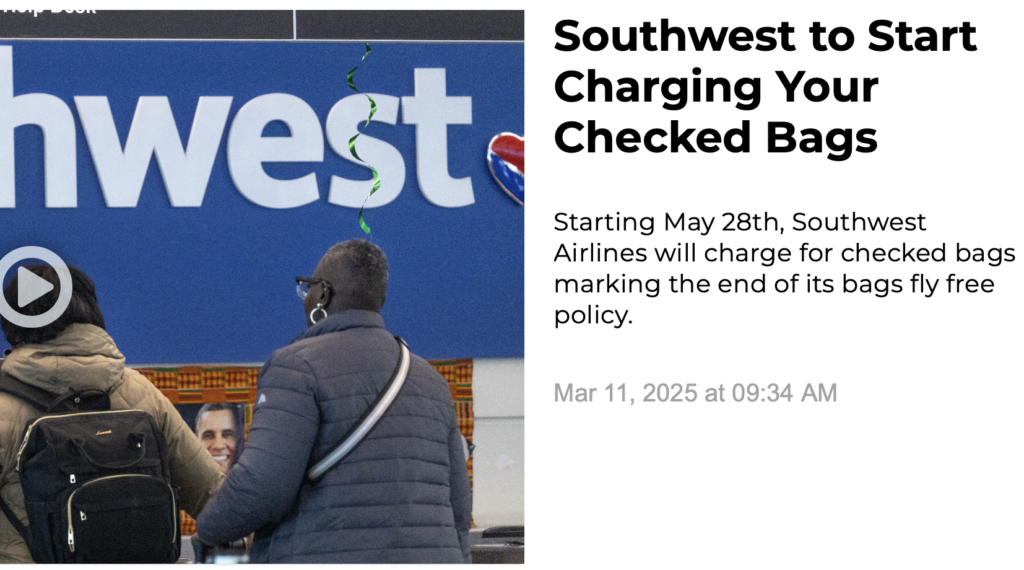

– Southwest sale: Book by today, fly between April 1 and June 11

*The Alaska sale includes Premium Economy, which is weird because Alaska doesn’t really support partner Premium Economy bookings for the partners you need to get to these destinations. #AlaskaGonnaAlaska - The Wyndham shopping portal has a bonus of 2,000 points after a single purchase through April 9. (Thanks to FM)

Don’t blame Rakuten, after all, Rasputin was once named Bryce right? (Don’t check)

{kind=link}