It’s been a couple of weeks since we talked about thinking about the velocity of money as an APR. As a quick reminder, when you make a spread for moving money around, you can think of the profit in terms of simple APR as:

APR = spread * banking_days / settlement_time

In the example from last time, a spread of 0.65% gave an effective simple APR of 54.6%.

Making it More Complex and Accurate

But, when you’re earning a spread, you’ve got that spread to invest after it’s paid out too which makes simple APR tell an under-optimistic story: Basically, if you earn $650 for moving $100,000, next time you’ll have $100,650 to move, so you’ll earn a bigger payout if you reinvest your earnings. Assuming you’re paid on some frequency we’ll call payout_frequency, we’ve got effectively a compounding APR (APRc) formula that tells a more complete story (editor’s note: if the formula isn’t rendering properly, check the web site here):

As my super annoying physics and math professors used to say in college, the derivation of that formula is left as an exercise to the reader. Of course it’s not super annoying when I do it, it’s cute right? Right?

Putting that all together with the numbers from last time, spread = 0.65%, banking days = 252, settlement time = 3 (avoid kiting), and payout_frequency = 12 (monthly), we get a compound APR of 70.6%. If you find a spread that pays out every time you move money, payout_frequency becomes 252 and, you’ll net even more with an effective APRc of 72.5%.

Conclusion

A small spread can look unappealing and make your brain flash a 🤏 emoji, but a small number compounded together a bunch of times can still turn into a big number. Obviously if you can do better than 0.65% on your spread of profit – fees (which you often can), then things look even better.

Happy Monday friends!

MEAB in a few decades; just like present MEAB, except older.

As a teen I worked at Albertsons for a year or two (and frankly sometimes I still feel like I work for them in a different, manufactured-spend like, capacity). One day on the job I loaded groceries into the trunk of a new car for a finance guy in a snazzy suit. He offered some life advice from the world of finance:

It takes just as long to do a big deal as it does to do a small deal.

– Snazzy suited finance guy

That’s absolutely true in most business deals, but often it’s not true in manufactured spend. For example:

You can sometimes send well into five figures using a bill pay service in 30 seconds

Waiting in line at Walmart to buy a $500 money order can take 10 minutes

Talking to a credit card company’s robot to try and push a payment through can take 6 minutes

Scrolling through a bunch of lame BankAmeriDeals double cash back offers for one that’s gameable (and will be hard to find) might take 5 minutes

So, I’d like to offer a suggestion: For any manufactured spend techniques you’re active in, start to build a mental model for two things:

How much time it’ll take

How much you’ll earn

With that mental model, you’re in a good position to know roughly what you’re wage per minute is for any given activity, and you’ve got a quick way to decide whether something is worth scaling or even worth your time.

At MEAB, we encourage churners to think about bank bonuses in terms of simple APR: for example, a $300 bonus on $30,000 deposited for 60 days is effectively an APR of roughly 6% (about $300/$30,000 * 365/60 * 100%). When savings accounts already earn 5.5% or above, this bonus almost certainly isn’t worth your time.

The Velocity of Money as an APR

The same rule applies for the velocity of money, even though no one really talks about it. What do I mean? Let’s assume you’ve got a simple rewards debit or credit card that earns a net profit of 0.65% for sending money through a FinTech (yes, this exists in myriad places in the real world). Assuming you can scale this, we’ve got a near perfect APR analogy for the velocity of money:

APR = spread * velocity

In this equation, velocity means bill pay cycles per year, or put more directly:

APR = spread * banking_days / settlement_time

Let’s take a concrete example: Assuming spread = 0.65%, banking days = 252, and settlement time = 3 (avoid kiting), we get:

APR = 0.65% * 252 / 3 = 54.6%

54.6% effective simple APR!

Conclusion

Moving money repeatedly with even a small spread has a huge effective APR, which you should keep in mind when deciding whether to park money in a high yield savings account, work on a bank bonus, or to scale your existing operations. Money in motion for a churner is often better than money at rest.

Happy Wednesday!

Next time on Wednesday Wisdom: Did you know that John Travolta = Nicolas Cage? This mug proves it.

EDITORS NOTE: In 2024, I’ve introduced Guest Post Saturdays. Today’s guest post is the second post in a series of at least two from the witty, inspiring, and definitely-not-a-giga-chad irieriley, his first post can be found here.

When to share the wealth

My grandfather was a gregarious man who loved more than anything to pass life advice down to his grandchildren. A lot of it centered around outlandish ways to get noticed in the job search (he once told me to send a pineapple with my resume inside to a hiring manager), but he also loved advice in the form of a good adage. His all time favorite is one we’re all familiar with: “irieriley, there’s no such thing as a free lunch.”

We’ve all accepted this as the truth, although MS and travel hacking allows us to get a consistent 90% off lunches, provided you are ready to decide on what you want to eat 355 days in advance. Therefore, it’s only natural to want to share this steep discount with family and friends.

Chances are, you’ve long been known as the “points expert” among your friends group and family. In my case, it’s so extreme that it’s generally the sentence after explaining my relation to the bride and groom in a wedding party bio.

And who can blame them? They see you agonizing over the choice of the Western or Japanese menu on ANA first or relaxing in the “base room” aka “bigger than a McMansion” at the Waldorf Ithaafushi and decide they want in on it.

However, most bright-eyed travel hackers aren’t going to hit the SUB on their first card, achieving breakage just like your favorite coupon book vendor intended. So, how best to set others in your life up for success? Here are some strategies that have worked well for me:

Provide starting direction

Not everyone is cut out to get super deep into the game, and that’s completely fine. There’s a plethora of reasons why it makes sense to target a SUB or two max a year. And thanks to the generosity of Chase and Amex, there’s generally always an elevated offer worth going for when your coworker Slacks to ask what card to get.

It’s a perfectly even exchange – you help people get a couple of free flights a year, and in return, you get fodder for Frustration Friday when they forget to use your referral link.

Add a partner in crime

Because of the collaborative nature of the hobby, helping your friends and family with the savvy to handle it can be a win-win.

I have a friend that I knew could make it as an advanced travel hacker, so I gave her some helpful hints a few months ago. I couldn’t be more proud of her progress, as she dove in head first and has already redeemed RT tickets to Asia for her and her P2.

If you have friends or family that can handle it, you’d be surprised how nice it is to have someone you know IRL to swap stories with.

Add P3, P4, P5 and so on

Most MEAB readers that are in a serious relationship likely count their significant other as their P2, since miles and points can be earned quite easily without all that much active participation.

It doesn’t need to stop there – some of us are earning and burning for much more than 2 players. This is more complicated than helping a friend and is a better fit for immediate family since it requires SSNs and financial trust, but it’s an amazing way to spread the wealth for those that have the time for it.

For what it’s worth, my P3 and P4 get stressed out about opening cards or the idea of MS, but they sure weren’t stressed when they flew Emirates first to Milan.

Book for them

For the truly advanced (or truly risk averse) earners out there, you can sidestep involving your loved ones in your shenanigans entirely and just let them enjoy the spoils.

Being able to treat family and friends to shared bucket list adventures or arrange emergency flights and hotels in a pinch are truly the most fulfilling way to use points.

This option can also be fantastic for things like group travel with your friends – a multi bedroom Vacasa is no big deal even post-devaluation when you’re earning 8x Wyndham on all of your “gas purchases”.

I’ll end by channeling my late grandfather with an adage – teach someone to use TPG referral links, and you’ll feed them for a day. Teach someone to responsibly MS, and you’ll feed them forever.

– irieriley

Pictured: DALL-E’s nightmarish rendition of my grandfather and I preparing the well regarded ‘resume in a pineapple’ method of standing out in the job search

I like to think I’m pretty good at spotting compromised gift cards; I’ve found and destroyed upwards of 1,000 over the last decade. In fact as far as I know, I’ve only actually purchased four compromised cards prior to last week. Then last week, my compromised card count increased by an eye-popping 25% (or 2,500 basis points because it sounds even bigger) when I bought a compromised Pathward Mastercard at Kroger.

Side note: I was already suspicious of that particular gift card because the security flap was too easy to remove, but the store had very low stock, I was in a hurry, and I was heading out of the country later that day, so I threw caution into the wind very stupidly. Don’t be stupid like me, and don’t be afraid to open a gift card in store and inspect it before buying it.

The Compromise

I opened the card in the parking lot, found a few clues that the card had been compromised:

The package was held together with super-glue

The CVV gummy was balled up

Removing the CVV gummy showed a scratched off code

The front of the card had four numbers scratched off

I know it may sound difficult to figure out that the card was compromised with nothing but those four clues, but luckily I did! So great.

When you have a compromised card, it’s a race against time to get it frozen and fixed before the card scammers are able to realize that the card was purchased and active, which is why it’s important to open and inspect cards as quickly as possible.

The Fix

I dialed the toll free number on the back of the card in my car at the Kroger parking lot, and I got stuck in Pathward’s automated call system. The system was repeatedly asking for a card number, and then hanging up on me after three failed attempts. I obviously failed every attempt because I didn’t have a full card number or CVV. Entering all 0s, 1s, or random numbers didn’t get me past the call tree, and neither did acting dumb and not entering anything either.

After a few frustrating minutes, I realized that another non-compromised Pathward Mastercard would have a valid number, so I got one of those and used its information, which got me through the automated system to talk to a human. The human was able to freeze the funds on the compromised card and issue a replacement by mail after looking it up using information on the barcode and about how it was loaded.

The Lesson

Gift card companies do their best to avoid talking to humans, and that means when a scammer scratches numbers off of cards, you may not be able to talk to a human when every minute counts. So, the point of this article:

On your phone, keep a list of gift card numbers, CVVs, and expiration dates for old, drained cards for every issuer and card type that you typically buy. Then, if you encounter a stubborn robot phone system, you’ll have quick information ready to get through to a human.

Happy Thursday!

Next up: Following the clues to decipher restaurant hidden messages.

It took me a few long-haul trips before I figured out the optimal length of a flight, here’s the logic I’ve arrived at for choosing the length of long-haul flights when you have options:

US to Europe or the Middle East: My optimal flight length is 10 ½ hours, long enough to take-off, sleep for 8 hours, have breakfast, and then arrive

Europe or the Middle East to the US: Typically you’re only napping when traveling this way, so my optimal flight length is the one that maximizes time on a wide-body and minimizes time on a narrow-body

US to Asia: Flights that leave in the late afternoon or early evening are best for resetting your schedule to Asia time

Asia to the US: Again, you’re probably only napping when traveling in this direction, so maximize time on a wide-body and minimize time on narrow-bodies

Happy Wednesday!

Next quick-tip preview: How to behave when visiting foreign tombs.

The American Express’s shutdowns from about a month ago rocked the community. Even though the total number of shutdowns was barely above the single digits, for about six hours, chat rooms, slacks, and forums lit up with discussion, data point sharing, and an impending sense of malaise. I was taxiing for takeoff for a week long international trip right when the news broke. Fortunately (?), I was able to stay connected with inflight WiFi to follow the drama in real time, and I was able to share in the myriad “what if” planning sessions that inevitably followed.

One of those “what if” scenarios was “what if I’m out of town with only one or two cards and I get shutdown?” There’s a simple mitigation:

Always carry cards from multiple issuers when traveling.

If I had been shutdown (I wasn’t), and if I only carried by American Express cards with me (I don’t), I’d have been in a rough spot. When I travel internationally, I carry a card from Chase, a card from Citi, a card from American Express, a card from US Bank, and a card from a local credit union. Some of those cards stay in my suitcase and some in my wallet. If and when I’m shutdown, I’ll be sad, but I’ll still be able to pay for things while I figure out next steps.

Special thanks to CF Frost for suggesting an article on this topic.

Occasionally adult advice from an occasional adult.

EDITORS NOTE: In 2024, I’ve introduced Guest Post Saturdays. If you’re interested in contributing, please reach out!Today’s guest post from community member George, who excels at automation, charity, and is an expert at bridging gaps. Donations for the 501(c)(3) non-profit Girls on Fire can be made online.

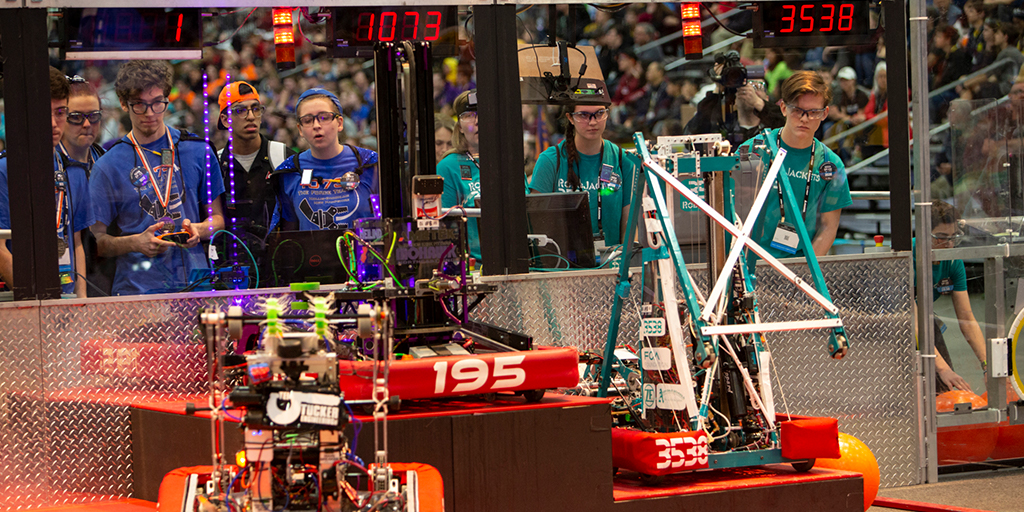

One thing I like to do in my free time, when I’m not working at my 9-5, churning, MSing, writing and sharing automation scripts for MSing, or going on trips because of churning and MSing, is mentoring student robotics teams.

Trust me, I’m going somewhere with this, and it’s probably not where you think.

You may or may not be familiar with FIRST, which is a global robotics community preparing young people for the future. My favorite thing about it isn’t the robots or the coding or the competitions but how diverse the program attempts to be in what it teaches. They say they are “more than robots,” and that’s definitely true.

One concept I particularly have learned to love is coopertition, which fosters innovation by promoting unqualified kindness and respect in the face of intense competition. I have been inspired by watching teams help each other during competitions and by helping other teams myself. Imagine Duke helping Carolina in the middle of the Final 4. Anyway, if you want to learn more, get in touch.

Now, here’s where I’m going: we should be more like these kids. We should cooperate.

Yes, there are reasons to be secretive in this game. It’s possible that if you give too much away, your plays will die out. However, have we run out of plays yet? Don’t new ones pop up all the time?

I’m not recommending radical transparency, but I do think we should share more. Certainly the more private and insular the group, especially if they are paid groups, the more information there is being shared. However, what credit unions were good for PPBP or what banks take credit card funding are still the kind of thing people often hold close to the vest. And again, yes, one just stopped allowing $15,000 in credit card funding pretty quickly after offering it, and that was probably our fault. But was that going to last forever without us? At least one person reports they were told that it was offered because of us.

Personally, I’ve found that at the right time and in the right venue, revealing sensitive information has come back to me positively multiple times over. Indeed, isn’t that the usual thinking when it comes to charity? Maybe you believe sometimes what you receive in return is some kind of “karma,” but sometimes, you get a new play from the person you helped.

Here’s what I recommend: next time you see someone, maybe someone new, asking for help…. help them. Oh, and if it isn’t obvious, this doesn’t just relate to churning.

Establish trust, then maybe give them a tidbit you wouldn’t share publicly. Even if they share it later, the chances aren’t so high that it will get out into the DOC comments or Reddit or wherever and ruin it, and if nothing else, you will have done a good deed. You may even get something better in return.

Waiting for a Chase Ink card application to stop spinning already.

{kind=link}