I’m not saying it’s a good idea, but closing a Bank of America card a month or two after meeting a retention offer doesn’t seem to cause any lasting repercussions on your account.

Stop & Shop and Martins have 8x points on Zift Zillions gift cards through Thursday, and Martins only has 6x points on DoorDash. Per-account limits are either $500 or $2,000 depending on the chain.

Meanwhile, sister brands Giant Food and Giant have 2x points on Mastercards for the same timeframe, limit $1,500 per account.

– $50 statement credit with $750+ online spend – $75 statement credit with $1,000+ online spend

The no-annual fee card remains unavailable for new applicants, and the likelihood of that changing is about the same of the US winning the World Cup this year. Go head and prove me wrong, Citi.

– Aeroplan miles can be redeemed for Hyatt Category 1-4 certificates “starting at” 25,000 miles – 50,000 Hyatt points can be redeemed for a 30,000 point Aeroplan reward certificate

– Aeroplan elites get a 20 night Globalist Hyatt status challenge – Aeroplan elites can convert Aeroplan to Hyatt at a 2:1 ratio – Hyatt elites will have an Aeroplan status challenge opportunity later this year

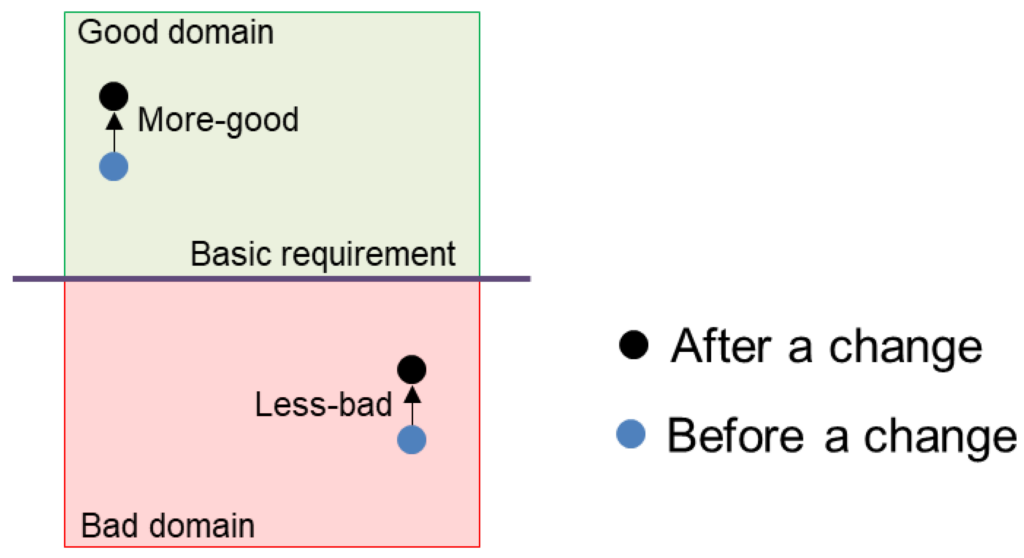

– Hyatt elites get an annual CAD $20 Aeroplan flight credit, which is worth approximately one gallon of milk at current exchange rates – Hyatt points transfer to Aeroplan at a less bad, but still bad, 2:1 ratio

On the positive front, that CAD $20 flight credit can be used to cover taxes on an award ticket, and on the uh-oh front, there’s now a backdoor from American Express to Hyatt.

Chase Ultimate Rewards has a 100% transfer bonus to IHG through July 30, bringing the transfer ratio from 1:1 to 1:2, which, like above, is less bad but still bad. On July 31, the bonus drops to 70% through the end of August.

Capital One’s non-Venture business cards have increased sign-up bonuses:

– Spark Cash: $1,000 statement credit + $250 travel credit with $10,000 spend in three months, annual fee is waived the first year – Spark Cash Plus: $2,000 statement credit + $500 travel credit with $30,000 spend in three months

For big spenders, the Spark Cash Plus is a monster with an additional 0.4x ($2,000) on every $500,000 spend and an annual fee refund after $150,000 spend.

– Marriott elites earn JAL FLY ON points – JAL elites earn elite status and stay based bonus points annually, but 🤏

I suppose FNBO hackers might now earn lifetime Bonvoy Gold too, which is probably worth at least $60 USD (or $6,000 TPG). Also if you like lighting money on fire and throwing its burning embers directly into a sewer, you can transfer JAL miles to Bonvoy at a 4,000:3,000 ratio.

Yesterday morning we chatted about Just4U’s 12x in-store DoorDash promotion, and yesterday afternoon multiple reports rolled in about 12x actually being 10x in true Just4U fashion. If you’re affected, customer service is manually crediting missing points – always check your receipt. (Thanks to Dawn for the nudge on a PSA)

Brex has a new $500 gift card bonus when signing up for one or both of a new Brex card or Brex business checking account in July. To be eligible, you’ll need to spend either $2,500 on your Brex rewards debit card or deposit $50,000 within the first 30 days. A few notes:

– Brex doesn’t like sole proprietorships – Brex likes tech companies, especially venture funded companies – Brex has interesting transfer partners and spend multiples, but transfer ratios aren’t 1:1

Brex can be down to clown as long as you tend to behave like a regular customer.

There might be a reason that a churning and manufactured spend blog is writing about DoorDash, and it’s not just about lowering the cost of expensive food.

It’s not too hard to spend $56,500 at grocery stores, gas stations, and drug stores in two months and American Express doesn’t care about cycling for seasoned accounts, so send it.

– According to the Javascript on the site, a promo code is two letters followed by nine numbers – Remember that zero is also a percent and opt for the alternate, zero bonus multiplier – Try and browbeat a Synchrony representative into a code

For no reason at all, here’s a friendly reminder that Synchrony cards shouldn’t be cycled, at all, ever.

A long useful travel hack is about to become less useful, so smoke ’em if you got ’em while you still can. Also, learn from this trick because travel hacking across different loyalty programs, or even different aspects within the same loyalty program, often rhymes.

– 45,000 points after $5,000 spend in three months – +1x points on up to $30,000 spend in six months

So, $30,000 spend is at least 105,000 total points, also known as enough for 1 ½ nights at Park Hyatt Kyoto or long enough to decompose (30 nights) at the Hyatt Place Lubbock. This will probably be available for referrals on Monday.

I got a rock, but it was at least a shiny rock this time.

Stop & Shop, Giant Food, and Martins have 10x points on Home Depot and Lululemon gift cards through Thursday. Per-account limits are either $1,500 $2,000.

It’s been a while, but the corporate overlords are punking the sister brand Giant with only 6x points.

SoFi launched “Smart Card Mastercard”. It’s not a credit card, but rather a charge card with spending limits set based on your assets in SoFi checking and savings. The vitals:

– $0 annual fee – 5% back at grocery (uncapped in theory) – 1% everywhere else (in theory)

Walmart, Target, Costco, and Sams Club are all explicitly excluded from the grocery bonus.