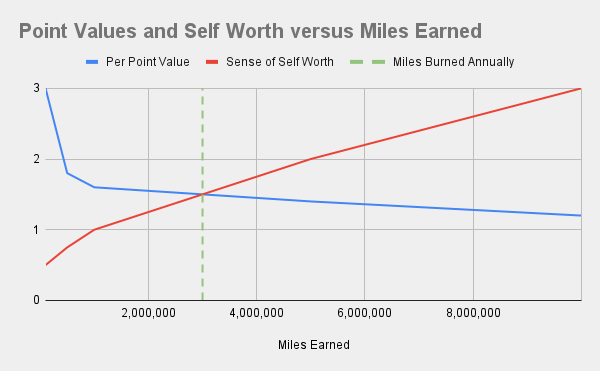

One of the hardest transitions between casual churning and becoming a heavy hitter is the switch from earning miles and points to earning cash back.

The transition should happen when you’ve earned all the miles and points you can spend cover your travel for the next 12-18 months, because:

Miles and points devalue by 30-50% in the span of years

The programs with the best redemptions change over time

Points don’t earn interest

The value of an unredeemed point is zero

Most of us don’t travel as much as we think we will (even if we travel a lot)

When you earn more points and miles than you can burn in a short time, the risk that excess points eventually become worth much less than when you earned them grows bigger than James’ Giant Peach from the famous historical documentary that I think is called “A kid finds a big fruit and someone wrote about it”.

Why do we fail to transition to cash back, even when we know analytically that it’s not the best option? The common answers I hear and that I’ve thought are:

Points and miles are fun, pennies aren’t

I’m motivated by travel, my job covers my cash needs

What if me and six of my closest friends need to fly Lufthansa F on last minute notice to Frankfurt and I don’t already have the miles banked, and my 800,000 Membership Rewards won’t post for another week?

They’re all valid reasons, but seeing them written can help prevent you from falling into the same trap. Trust me, you don’t want to be down 100,000 Hawaiian miles that expired a few years ago because you didn’t ever have an actual use for them and weren’t active in the program; $1,000 would have been a lot better. #askmehowiknow

– 20,000 Membership Rewards or $200 statement credit after $1,200 spend on Virgin Atlantic through November 30 – 20,000 Membership Rewards or $200 statement credit after $1,000 spend on AirFrance or KLM through December 31

It’s too bad the Virgin Red Synchrony Mastercard isn’t somehow also involved but that’s probably because it hadn’t been invented yet when AmEx cooked up the offer, at least according to what I just made up. (Thanks to FM)

As we all know, what’s even worse than a Frontier flight? More Frontier flights, that is unless you want to fly Des Moines, Iowa direct to Guadalajara Mexico; Frontier is the only airline that has that flight in the bag.

Marriott has a similar deal with AirCanada Aeroplan with a smaller bonus that works out to 28,000 miles, which frankly is worth about the same as 36,000 MileagePlus miles. Frankly I’m impressed at some marketing person’s mileage valuation prowess.

The Pepper gift card platform, seemingly created as a conduit for moving money between venture capital bank accounts and gamers’ wallets, warrants discussion based on recent developments and crowd think.

Background

Moochoo, the company, the company behind Pepper, raised $23.05 million on December 21, 2023. Is it auspicious that they closed on a pagan holiday? Probably not, but it’s funny. Pepper’s go-to-market strategy started shortly thereafter with effectively unlimited 10% back (in Pepper coin currency) on new accounts for the first 15 days of the account’s existence, along with bonuses for the referrer. They appeared to want new users at all costs and turned a blind eye to gaming with zero due diligence on new accounts. (Have a new device? That’s a new person, obviously. It’s not possible to have more than one, duh. Just make those charts go up and to the right!)

Seven months later in July, Pepper pivoted its rewards scheme away from unlimited new account cash-back, almost certainly because at its then current burn rate, it wouldn’t survive long in the face of unlimited purchases of Walmart, Home Depot, Amazon, and other high value gift cards at ~90% of face value. Pepper replaced the new-user sign-up bonus with double base points on gift cards for the first 15 days, which wasn’t useful for bulk resale and caused volume to plummet. How do I know volume plummeted? Pepper order IDs are sequential, naturally.

The Now

Pepper took a few weeks, but they’ve settled into the new normal. Now, they release “Daily Boost” merchants once, twice, or three times a day. Boosted merchants earn much more than regular, like 12x on Amazon or 20x on Columbia Sportswear. Boosted merchants have a total capacity before the boost goes away, which sometimes happens in 30 minutes for popular brands and sometimes doesn’t happen at all.

The Warning Lights

There are a few recent developments that could be taken as warning lights:

Boosted merchant rewards payouts are now delayed by several weeks (is this related to cash-flow concerns?)

New accounts now require ID scans, but only as of a few weeks ago (why now, maybe because they’re trying to raise money and VCs want real user verification?)

Boosted merchant deals are getting better brands and higher payouts daily (why offer bigger than 10% discounts on high-volume bulk resale gift cards like Amazon, Walmart, and HomeDepot, which were probably burning Pepper’s cash reserves down like a dry Christmas tree on fire? Maybe to build temporary operating revenue?)

The capacity for boosted merchant deals seems to be increasing steadily (again, is this for cashflow reasons?)

Boosted merchant deals seem to be shifting to the brands that sell-out quickly from the brands that don’t (why push for more volume on cards you’re probably taking a loss on?)

To answer these questions, I think it’s time to build a simple quant-model for Pepper’s cash reserves.

The Pepper Doomsday Countdown

Let’s come up with a model for how much cash Pepper probably has left. The formula is really just $23.05 million, minus burned cash, plus earned profits. Let’s make some data-driven assumptions:

Monthly operating expenses, salaries, and benefits for 37 employees, assuming an average overall employee expense of $65,000 per year (this is likely a rather low estimate): 37 * $65,000 / 12 = $200,416 / month

Number of transactions through September 30, 2024 (order ID’s are sequential): 857,000

Average transaction size (bulk brands are usually between $750 and $1,500 in max size): $1,000

Monthly profit from regular discount gift card purchases for non-boosted accounts and users, assuming 3% profit: 3% * $500,000 = $15,000 / month

Per order losses on boosted transactions, assuming 3% loss: $1,000 * 3% = $30

Percentage of transactions that are boosted, in a new user sign-up bonus, or otherwise money losing: 80%

Now, let’s run the America-Loves-Math-o-tron-5000:

So, ~$23 million raised and ~$22 million in expenses by my simplistic toy model. You can play with the numbers and come up with your own conclusion, but you have to get pretty far below a 3% per transaction loss to make things look rosey for Pepper, or really far above $500,000 per month in profitable transactions.

Where does that leave me? I think Pepper is about 10% likely to die in the next 30 days, and maybe 50% likely to die by the end of 2024; unless of course they find another VC that wants to shoot money into a toilet. I’m still playing the Pepper game but only at a small level. If they fold and I lose my floated Pepper rewards, I’ll live without much regret.

Happy weekend I guess?

The result of the last round of Pepper’s VC money cannon.

The effective APR of this deal is 13.3% in the best case or 10.0% in the worst case, but the real reason to do this is for opening up Bank of America credit card approvals. (Thanks to DDG)

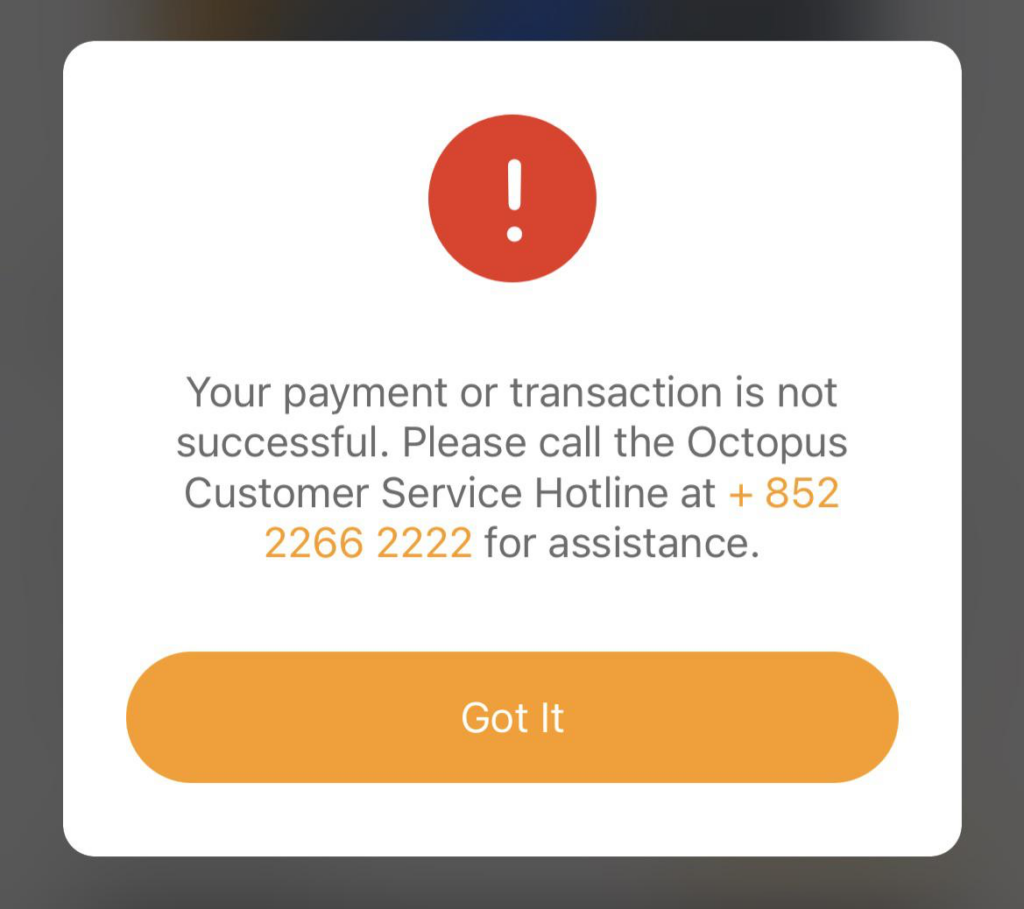

Chase’s Q4 Pay Yourself Back 25% bonus categories are: utilities, insurance, fitness clubs and gyms, gas stations, and annual fees. Bonuses are all only the Sapphire Reserve this quarter too. “Select Charities” remains at its 50% bonus value. So long high volume gold cash-out, but hello octopus insurance cash-out!

– $300 travel credit resets in December as usual for use past your December statement – Remainder of unused December credit becomes a statement credit on December 31 – $300 travel credit for January 2025 – [your anniversary date] – $300 travel credit for [your anniversary date 2025] – [your anniversary date 2026]

I think this means a bonus $300 travel credit in 2025.

Chase’s has a few targeted promotions for booking through the travel portal:

– 10,000 bonus Ultimate Rewards after booking a hotel stay of $400+ by January 31 (via email) – $100 back on $500 in spend by October 31 (via Chase Offers)

These will stack, and these are (probably) both gameable. (Thanks to FM)

Pay yourself back hiccups when buying Octopus insurance.

This one is safe for anyone to use, potentially unlike the one made public last week which was dubious at best and err, scary at worst. Why was that one dubious? It was a manufactured link specifically constructed with two contradicting offers that happened to pass through the application system in an unintended way. Side-note: That fact that this link is dubious still isn’t noted on other blogs, hopefully because they just don’t know. Always know the province of links before diving in. (Thanks to reb702)

I got approximately 25,000 Rapid Rewards points back by grooming by existing bookings, though most of those existing bookings are backup flights so the expectation value for my actual cost is lower than 40%.

There’s a ton of economy space at 15,000 miles in this month’s drop, more than I’ve ever seen in-fact. Discount business class space is almost non-existent this year and barely-existent next year.