This week is bound to be a little slow after the Memorial Day frenzy, but there are still deals coming, keep your heads up:

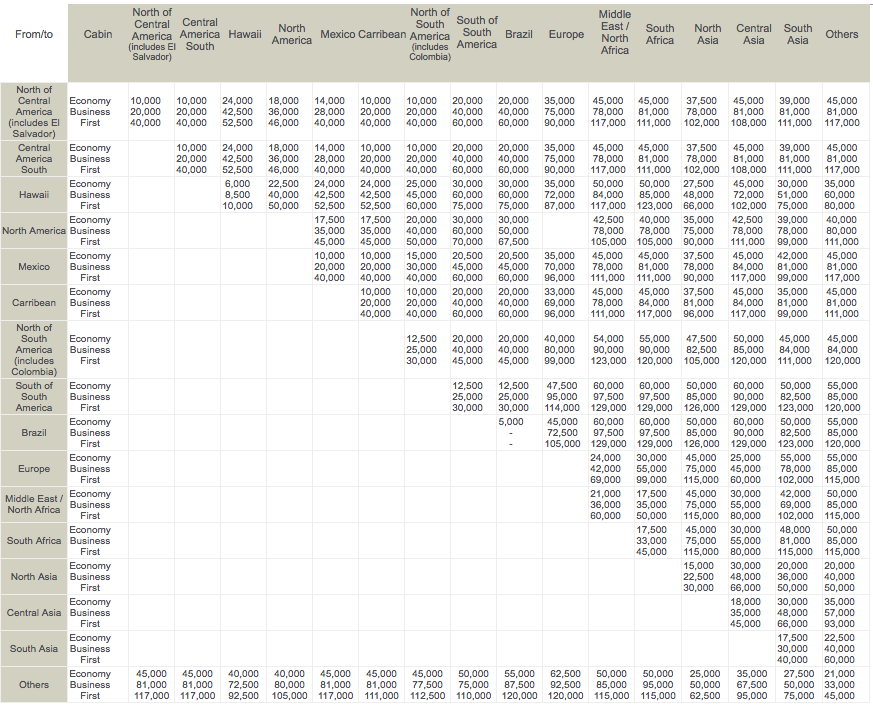

1.Brex has a 25% transfer bonus for Avianca LifeMiles running through July 2, 2021. The LifeMiles award chart has some sweet spots, and it’s a currency that’s been extremely hackable and currently still is mostly hackable. The current award chart has relatively decent prices to Europe at 63,000 miles for Business class or 87,000 miles in International First class, with lots of availability through Star Alliance partners. AwardWallet has a nice tabular LifeMiles Partner Award Chart, and region definition to help you strategize.

Hint: A lot of the value in LifeMiles comes from their definition of a region.

2. AA has a portal shopping bonus of 1,000 miles for installing their browser extension toolbar and spending $25 at a supported merchant between now and Friday. I’d do this in a separate browser and disable the extension instead of uninstalling it so they don’t get notification that it was removed. (Alternatively, you can disconnect from the internet and uninstall for the same effect.)

If you have normal shopping, do that. Otherwise, I’d just buy an ebay $25 gift card at GiftCards.com and sell at 90%, which will earn you 1,000 AA miles for a cost of $2.50. At that rate I’d buy a million AA miles, seriously.

Keeping our heads up for deals falling from the sky.

Unless you’ve been stranded on a desert island all weekend, then you’ve almost certainly heard about the Chase Sapphire Preferred’s 100,000 point sign up bonus because it pays affiliate bloggers a hefty commission when you open a card with their link, and in fairness it is indeed a historically high sign up bonus (my link is not an affiliate link, it’s not my style). Should you go for it? Maybe, but it’s definitely not the best thing that happened in travel hacking since AA retired its torture-tube E-140 fleet. A few things to consider about the card’s 100,000 points:

You’ll have to be under Chase’s 5/24 limit to even get the card, with or without a bonus

You can’t have earned a Sapphire sign-up bonus in the last 48 months

You can’t currently have a Sapphire product open

This is only 10,000 points more than the current usual 90,000 points offer, hardly something to write home about UPDATE: Harv notes that 80,000 points is the usual offer, thanks for the correction

That last bullet is of particular note. You can get multiple Ink Preferred cards (even in the same week), they earn the exact same Ultimate Rewards, they don’t count against 5/24 when opened, you don’t have to worry about them showing up on your credit report, you get essentially the same benefits as the Sapphire Preferred, and they’re honestly pretty easy to get as far as Chase cards go. You can product change them to a no annual fee Ink Cash for 5x at office supply stores when the annual fee hits the second year too. Even better, Chase regularly targets business owners for 125,000 Ink Preferred sign up bonuses by mail or just for asking a banker in branch.

So, if you’re excited for the 100,000 point Sapphire Preferred bonus and it still fits given everything, by all means go for it but make sure you do the Chase Modified Double Dip which will earn you 160,000 points rather than getting the Sapphire Preferred 100,000 points by itself. Otherwise though, maybe consider opening an Ink Preferred or two instead.

Where you’d have to be to not have heard about the Chase Sapphire Reserve sign-up bonus.

In this hobby we’re really good at moving money around from bank a, to credit card b, to debit card c, then maybe back to bank a. We’re also good at parking money in accounts for a $750 bonus at Bank of the West or a $600 bonus at HSBC. If you’re like me, that means large sums of money are occasionally sitting in bank accounts, partially as a cushion for lax record keeping in order to avoid overdrafts in case you forget about a pending ACH or charge, and partially as a holding pen for sign-up bonuses or other perks. (And let’s not talk about the stack of gift cards waiting to be liquidated on my desk on any given day.)

When you’re letting money sit you’re subject to the opportunity cost of what that cash could earn if you didn’t leave it parked in some rando bank account. That money could instead be invested in high interest checking accounts (3-5% APR can be had with just a little bit of effort and some scheduled Plastiq $1.00 payments or with Debbit), maybe in US Treasury bills, perhaps you could be putting your money into buying Playstation 5s or graphics cards for resale, or you could be actively or passively investing in the stock market. All of those things will (hopefully) earn you money, and it’s quite likely that you’ll earn more money in those vehicles than the almost nil interest rate your bank probably pays. You’ll potentially earn more than you’re getting with sign-up bonuses too.

MilesEarnAndBurn Case Study: I’m a 90% passive index fund investor (VTI and VEU if you must know) with the other 10% being my own active stock picking based on fundamental market value and a very small smidge of speculation. I’m often right enough about my active stock picks that my 10% allocation grows to be 12% or 14%, so I rebalance back to the 90/10 split and keep going. What does that tell me? If I had a smaller cushion in my bank accounts and better record keeping about money flowing around, I’d have more money for investing, which will almost certainly outperform my stupid 0.005% APR checking account returns in the long run. I’m costing myself real money with my current strategies. I can and will do better.

Takeaway: Pease take a few minutes this weekend to think about your cash, how it sits and how it flows, and whether you’re using it in a way that you’re happy with. Don’t discount that there’s inherent value in simplicity too, if it’s just easier to let an extra $10,000 sit at a bank account to avoid the mental load of more strenuous record keeping, so be it. To be sure, I’m not suggesting any one particular investment vehicle or investment strategy — do what works for you, but please make sure what you’re doing is intentional.

A representation of how I’ve failed my bank account.

It’s one of those weird holiday weeks where Monday seems like Sunday, Wednesday seems like Friday, and Citi seems like its servers consist of MS-DOS and Windows 95 machines running in a shed in rural Ohio. (One of those things is true.) Here are three to carry you toward Friday: (or is it Saturday?)

Point.app posted my Amazon 10x points bonus for buying a gift card as expected; what I didn’t expect was that they’d stack the normal 3x at Amazon on top of it.

Now, they’ve got a $30.00 cash back / 3,000 point “streak” offer for using the card for 5 days in a row with an aggregate purchase size of $100. They’ve also got a 5x offer at BestBuy, both promotions run through June 13. So buy a $100 BestBuy gift card and then use Debbit for 4 days to make a $1.00 transaction automatically; you’ll earn $39 in points for spending $104. If you don’t have Point.app, find a referral link from a friend and you’ll both earn $100 back.

Register here for 25% back on Hyatt award stays between June 15 and August 20 at JdV, Destination, or Unbound Collection Hyatt hotels if you have the Chase World of Hyatt credit card. If any of those brands line up with your travel plans already, 25% is a great incentive. I’d suggest registering even if you don’t currently have plans in case you end up at one of those hotels before August 20.

In what seems to be a recurring theme for 2021, another airline is having an anniversary contest in an attempt to generate marketing buzz, and, unfortunately, it’s working. (It worked for AA and United too.) Who’s next? If it’s a big US carrier, the only real option is Delta. I’m resolving right now to not fall into writing about a Delta anniversary scheme because at least once this year I don’t want to be played by an airline’s marketing department.

Anyway, Southwest has a 50th anniversary game going between now and June 18 at this link. You can enter once per day per Rapid Rewards account. My P2 won 50 Rapid Rewards points and I won nothing and got played. (That said, I did end up winning about 18,000 miles in the AA sweepstakes, so I will be playing this Southwest one daily, unless it plays me, amirite?)

Live capture of Southwest’s marketing department scheming.

I hope your Memorial Day was as nice and relaxing as mine was. Since I didn’t scour the churning space this weekend like I normally would, I’m going to offer your a generic tip instead:

American Express doesn’t do a hard credit-pull for almost all applications, successful for rejected, as long as you have at least one of their cards currently open. That means that sending in applications for American Express cards (especially business cards because they won’t show on your credit report) is pretty much consequence free. If you’re not lobbing in an application for an American Express sign-up bonus every few months, make sure you’ve got a good reason for it. With an average sign-up bonus sitting north of 90,000 these days and four successful business applications a year, you’re looking at 360,000 bonus membership rewards points with absolutely zero impact to your credit score. That’s a big deal.

My majestic Memorial Day wind-surfing experience. That’s one foot on the board people, I’m basically pro.

{kind=link}

{kind=link}