We’ve seen a wave of shutdowns for heavy hitters from both Chase and American Express since Friday. The two banks shutting down at around the same time seems coincidental, but it’s a double whammy for a few manufactured spenders. We can talk about the reasons behind the shutdowns later, but there’s an important lesson that it’s time to reiterate:

Burn your points early and often. When you’re shutdown, you may lose them altogether.

I can only assume that you don’t want to be the guy stuck with 80 million Membership Rewards that were just confiscated, but you know what they say about when you assume.

Different deals look differently, but those involving a credit or debit card usually involve a loop like:

Buy a virtual or physical thing

Earn rewards (probably)

Pay fees (probably)

Liquidate the virtual or physical thing

Earn on sale (rare)

Pay commission or fees (probably)

Use the money to pay your credit card

Earn rewards (rare)

Pay fees (rare)

Your profit is (probably) obvious: Add up all the rewards and sale price, then subtract all the fees or commissions and purchase price. Assuming the deal scales, you’ve probably got a nice play.

But, let’s get to the real point: what’s the limit of how hard you should abuse your card to complete this loop? Wander there with me friends by asking a roundabout question: How much would the issuer need to pay you to close your relationship with them?

For a small credit union, you’d probably severe a relationship ]for a few (tens of?) thousands. For someone who loves staying at Hyatts and routinely books points boost outsized value fares through Chase Travel, you might theoretically need six figures or more to close that relationship. And that brings us to the answer, sort of:

Don’t push a card so hard that you’ll lose it, unless you’re going to make more than the issuer would have to pay you to terminate your relationship.

At least we got there. Have a nice weekend friends!

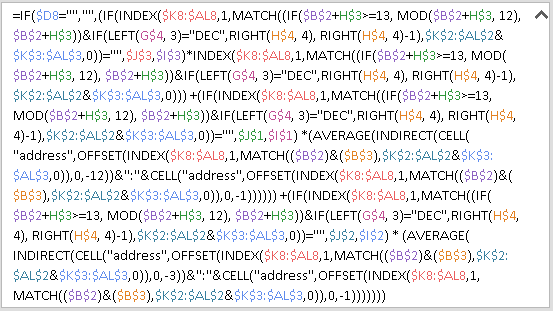

Helpful tip: This excel formula can also help you answer a question.

Churning and manufactured spend is easy when every electronic payment lands, every cashier is cooperative, category multipliers multiply, Toby’s too bogged down with lawsuits to look at you, and none of your accounts meet the almighty axe. Building plays, forming loops, and increasing velocity is child’s play when everything works.

The problem is that in churning and manufactured spend, Gene Kranz’s edict of “failure is not an option” is, uhh, not an option. Something will fail and it’ll probably take multiple phone calls and multiple people to get it fixed, if it’s even fixable. To build longevity in the hobby, have a backup plan for when:

Your bill payments get lost in the ether

A FinTech decides to hold your $200,000 in deposits

A credit union shutdown causes a bounced payment to American Express

Your loyalty points end up in an orphaned account

What does that backup plan look like? It really depends on the failure mode, but at minimum you should have the funds to sustain everything if an account is closed or frozen, you should have more than one account set up for making payments to your credit cards, and you definitely shouldn’t wait for things to fix themselves instead of getting on the phone and straightening things out as soon as you can.

Happy Wednesday!

Backup plans don’t always look the way you think they should.

Plays are always evolving and as plenty of us have learned, they can vanish in the blink of an eye. That’s especially true if you’re a believer in axe-everything-Saturday, but I digress. When a play inevitably dies for you, you’ll need to pivot to a new play. If you’re like many of us, that takes time with roadblocks like:

Analysis paralysis, like “what’s the best way to get money into that new account?”

Fear of another shutdown, or “but what if this new play gets me shutdown at my credit union?”

Setup friction, or “I need a new EIN and some micro-deposits, I’ll do that later”

Opportunity cost, or “I could just run over to Kroger instead”

I’m sure you’ve got a few more to add to the list too. The punchline here should be obvious, when you let roadblocks get in the way, you’re not earning money on a new play. Since plays can die in weeks or months, getting six to seven figures through them in a short time can be the difference between earning lunch money or earning a new SUV.

Good luck friends!

Then there are the plays that earn “lunch” money instead of lunch money.

Taxes and manufactured spend are often intertwined and given that taxes are sort of due tomorrow, let’s focus on some churning centric tips. Before that though, it’s time for my periodic reminder that I’m not a financial professional and I’m definitely not your financial professional, but I do know how to spell professional without autocorrect so that’s something.

So, let’s start with deadlines:

Your 2025 tax return or extension is probably due tomorrow

Your 2025 tax bill is probably due tomorrow

Your 2026 Q1 estimated taxes are probably due tomorrow

Next, information on payments:

You can pay taxes with a credit card or debit card

Churners have lots of 1099s because reasons, and when there are lots it’s easy to miss one. If that sounds like you, consider waiting until June for your IRS transcript to be fully populated and use it to cross reference your paperwork

Not all 1099s have taxable income, and not all taxable income has a 1099

Good luck, and I’m sorry for the time-suck you’re going to have to endure dealing with this.

EDITOR’S NOTE: Yes, we can be silly around here. However, April 1 is somehow the sanctioned silly day for the rest of the world so of course it’s the one day that strait-laced seriousness takes over at MEAB. You can get your weird Bonvoy and Delta hidden value fake posts elsewhere I’m sure. #sorrynotsorry

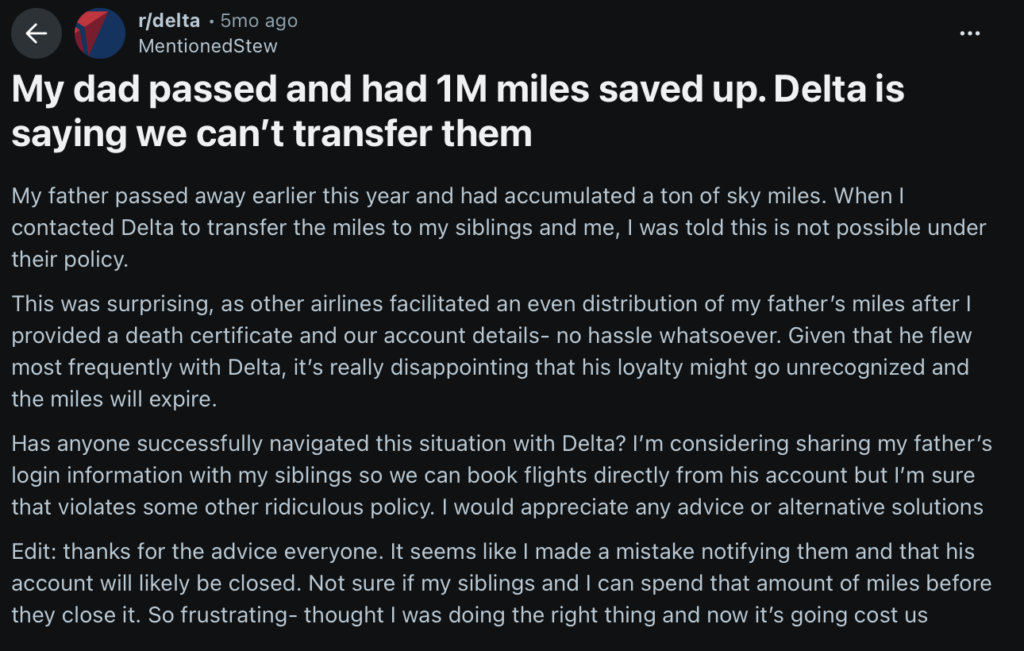

The General Rule

Points and miles held in loyalty programs are a real asset, even if they’re worth less over time (even worse than holding cash). If a loyalty program member passes away, most programs’ terms and conditions forfeit the value of their loyalty account completely and the account is (in theory) effectively worthless. So as a general rule, when you or another player dies, remember:

Don’t tell the loyalty program when a member passes, rather just cash-out or redeem points as quickly as reasonably practical.

The Nuance

The general rule doesn’t apply everywhere, not every program has blanket forfeiture. The US exceptions:

Alaska has an unofficial “Memorial Miles” process to transfer, contact customer service

Its “own discretion” shows up a lot there, I’d consider whether you really want to trust Toby’s discretion before moving forward.

The Practical Side

None of the loyalty programs that transfer points will transfer elite status, upgrade certificates, club access awards, tier awards, elite qualifying points, or similar, and each of these things has value, potentially thousands of tens of thousands of dollars worth. So, probably just keep following the general rule when you can even if the program lets you transfer.

Special thanks to Churnest Hemingway for today’s guest insightful guest post. Watch soon for his upcoming novel, The Old Man and the Fee.

When communicating with groups in person or online, one of the most important questions you can ask yourself is “Who’s in the room?” Knowing your audience and understanding their agenda (tip: it’s different than yours) should shape what you’re saying, and validate why you’re saying it at all.

This advice is also very relevant for communication about churning. Whether discussing a card benefit loophole or a foundational tool for manufactured spending, you should always stop to consider who is in the room before starting a conversation – lest you also start the death clock on the very play you’re hoping to discuss. We have seen this lack of discretion contribute to the demise of many joyful things in recent years, sometimes in conjunction with quantitative signals, sometimes not.

If you’re posting to reddit, commenting on a blog or video, or publishing content yourself, you can be confident that the marketing departments of major credit card issuers are reading what you’re putting out there. Marketers report up to other departments on product usage trends and the voice of their customer. If the voice of their customer is yapping about a loophole its not supposed to have, a feature its not using as intended, or anything else of benefit beyond what is advertised, you can be certain those goodies will be killed by product leadership sooner or later.

Similarly, when chatting or on the phone with your friendly customer service rep, you should be aware that everything you say is being logged and analyzed in dashboards, meetings, and meetings about dashboards. Just as with marketing departments, surges in specific topics or questions stick out on the radar like a sore thumb. Badgering a bank employee about a key account feature that was retired will not magically turn that feature back on. Over a hundred of these calls will raise the question of why this feature is suddenly in demand, and prompt further investigation of customers who still have skin in the game.

Sharing away from the corporate eye does not guarantee privacy, either. Smaller online communities have their own share of participants who repost tips and plays without adequately gut-checking what it means for the survival of what they’re sharing. Some of these are from well-meaning churners excited to share knowledge with their peers and build community. Less forgivably, lurking influencers capitalize on community content by monetizing it for ad-supported blogs and paid courses. This latter demographic is a scourge and the reason you should know the agenda of your peers.

Finally, a common thread between all three audiences is the new variable of AI analysis. Every reddit post, chat or call log, or private community message is now subject to any number of agents ingesting, synthesizing, and summarizing its content ad infinitum. Despite bank technology having a reputation for being old and brittle, it is simple enough to batch export data and analyze it with another application. Many churners also use these tools, undisclosed, in private communities to manage the firehose of information coming at them on a daily basis. Even if you’ve forgotten what you once posted way up in the scrollback, or are past the 90 day window of your visible Slack content, don’t worry – AI remembers, and will always remember. The act of listening has now been delegated to a technology that never sleeps. Proceed with caution.

A footnote: “X has already been shared by popularwebsite, so it doesn’t matter if I share it again” is not a good excuse for indiscretion. Visibility on a play doesn’t come from one leak, but repeated signals indicating its heat and significance. Even if a play has been shared that cannot be unshared, abstaining from a repeat broadcast is good practice for extending its lifespan and diminishing its significance to those who would treat it indelicately – or those who have the power to see it killed.

So, what should we do when we don’t know who to trust? Build trust. Know who’s in the room by getting in the actual room. Get on calls, show up at meetups, and build churning relationships that turn into churning friendships. Gracefully retract and delete overshares when other churners let you know you’ve gone too far, and give a polite nudge when you see someone else spill too much (escalate as necessary). Despite only knowing each other by first names at best, the amount of trust in our hobby is uniquely special, and the only thing that keeps it together.

I’m an optimizer; frankly, I think most of us are or we wouldn’t be doing this on a day to day basis so I guess misery loves company, right? We’re all rather adept at optimizing credit card category spend multipliers, payment windows, new application timing, and new account bonuses.

Optimizations aren’t perfect though and it’s easy to get stuck in local minima. I regularly see newbies and experienced churners alike make an optimization mistake with their time: spending minutes or even hours chasing a deal that’s not worth very much. An extremely successful salesman once gave me some simple advice:

It takes about the same amount of time to do a small deal as it does to do a big deal.

The obvious lesson is to spend your time on bigger things instead of on smaller things. An alternative way to think about this is to consider the minimum you need to make for different manufactured spend and travel hacking opportunities, and don’t bother with the ones that don’t have a big enough return on time. To that end, I’d suggest having a mental set minimums, much like pilots have a set of weather minimums. In case you’re a visual learner, here’s a sample table that you can fill in for “fun”. For extra “fun”, compare with your neighbor:

Activity

Minimum Profit Needed ($)

Leaving home for in-person manufactured spend

Manufacturing spend at home (something quick)

Manufacturing spend at home (something less quick)

Calling customer service for a retention offer

Tracking a card linked offer over couple of months