– Explorer: 70,000+10,000 MileagePlus miles after $3,000 spend in three months – Quest: 90,000+10,000 MileagePlus miles after $4,000 spend in three months – Club: 100,000+10,000 MileagePlus miles after $5,000 spend in three months – Business: 100,000+10,000 MileagePlus miles after $5,000 spend in three months – Club Business: 100,000+10,000 MileagePlus miles after $5,000 spend in three months

These are generally available via referrals, so please use a referral link.

– Deposit $25,000 within 30 days – Maintain at least $25,000 balance between days 30 and 60 – Make at least six transactions by day 60 (Six $1 ACHs do nicely)

If you manage your money perfectly, this is effectively a 72% annualized APR, which is almost 72% more than what Chase business checking will give you. Even if you’re not in US Bank’s footprint you can still do this, just open a different relationship with US Bank first. T&C here.

Bank of America has credit cards available via the Rakuten shopping portal:

– Travel Rewards: $150 from Rakuten plus 25,000 points after $1,000 spend in 90 days – Customized Cash: $75 from Rakuten plus $200 after $1,000 spend in 90 days

The business versions of the cards have higher offers than the portal and sign-up bonus put together, so keep your enthusiasm appropriately calibrated. (Thanks to DoC)

JetBlue raised bag fees a couple of days ago. I didn’t mention it because I was sure the list would grow within the week, and indeed it’s happened. So now we’re at:

AA, Alaska, and Delta are sure to come in the next week, but they’ll stagger it for optics. Who says there’s collusion in the industry? This is just about fuel, duh.

The AmaZing Business Visa card has an increased $1,000 sign-up bonus or 100,000 point sign-up bonus depending on the version, but is only available in some states:

Underwriting is a manual process, and there isn’t actually a difference between the points card or cash back card other than the extra step to redeem your points for cash back.

The Bank of America Alaska Atmos cards have new offers different than the new offers from a few days ago:

– Summit: 100,000 miles and a 50% flight discount after $6,500 spend in 90 days – Ascent: 80,000 miles and a 50% flight discount after $4,000 spend in 120 days – Business: 85,000 miles after $5,500 spend in 90 days

The 50% discount has to be flown between September 8 and November 18 with lots of other asterisks, so cool I guess. (Thanks to Jerry)

– Gift card face values must be in multiples of $50 – One credit card per gift card purchase – One gift card per customer per day

These aren’t implemented at the register level though, so your success level may be tied to your rizz level. Data points specifying rizz are needed to confirm.

March’s Chase Air India offer for 10% back on $100-$500 in spend has a new, April version. The March warning still applies: The best game for this one is to not fly Air India under any circumstances, ever, which should make your game clear.

EDITOR’S NOTE: Yes, we can be silly around here. However, April 1 is somehow the sanctioned silly day for the rest of the world so of course it’s the one day that strait-laced seriousness takes over at MEAB. You can get your weird Bonvoy and Delta hidden value fake posts elsewhere I’m sure. #sorrynotsorry

The General Rule

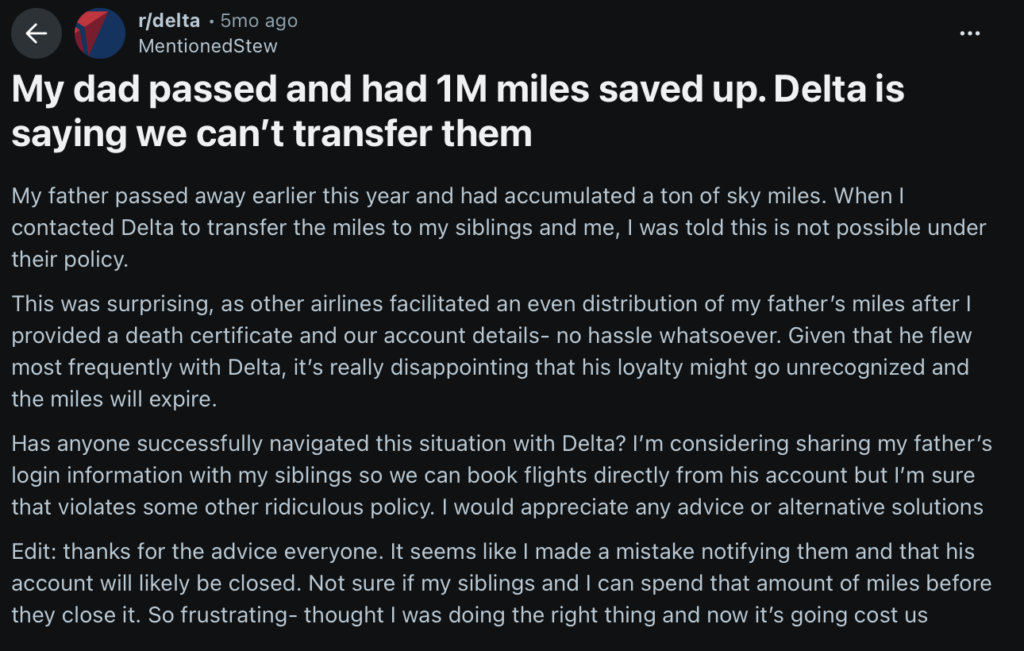

Points and miles held in loyalty programs are a real asset, even if they’re worth less over time (even worse than holding cash). If a loyalty program member passes away, most programs’ terms and conditions forfeit the value of their loyalty account completely and the account is (in theory) effectively worthless. So as a general rule, when you or another player dies, remember:

Don’t tell the loyalty program when a member passes, rather just cash-out or redeem points as quickly as reasonably practical.

The Nuance

The general rule doesn’t apply everywhere, not every program has blanket forfeiture. The US exceptions:

Alaska has an unofficial “Memorial Miles” process to transfer, contact customer service

Its “own discretion” shows up a lot there, I’d consider whether you really want to trust Toby’s discretion before moving forward.

The Practical Side

None of the loyalty programs that transfer points will transfer elite status, upgrade certificates, club access awards, tier awards, elite qualifying points, or similar, and each of these things has value, potentially thousands of tens of thousands of dollars worth. So, probably just keep following the general rule when you can even if the program lets you transfer.

– Synchrony will axe you if you cycle this thing, though it may take a few months – Categories on this card are weird, but typically weird good not weird bad – The targeted offer isn’t at Venmo.com

Your Venmo account will survive if your card is axed. Oh, and at the risk of taking more flak, the sites that “always show you the best offer” don’t seem to be showing this offer… yet?

The Bank of America personal Alaska Atmos cards have increased sign-up bonuses:

– Ascent: 85,000 miles after $4,500 spend in 120 days. – Summit: 100,000 miles after $6,000 spend in 90 days

Why no business? I’m not sure, wait for April 1 I guess.

These are Pathward / BlackHawk Network gift cards.

There are multiple reports that Cardless now allows holding three cards. You can’t get the Celtics card anymore, so just make sure you dial back that enthusiasm by 8x, or is it 6x?

Special thanks to Churnest Hemingway for today’s guest insightful guest post. Watch soon for his upcoming novel, The Old Man and the Fee.

When communicating with groups in person or online, one of the most important questions you can ask yourself is “Who’s in the room?” Knowing your audience and understanding their agenda (tip: it’s different than yours) should shape what you’re saying, and validate why you’re saying it at all.

This advice is also very relevant for communication about churning. Whether discussing a card benefit loophole or a foundational tool for manufactured spending, you should always stop to consider who is in the room before starting a conversation – lest you also start the death clock on the very play you’re hoping to discuss. We have seen this lack of discretion contribute to the demise of many joyful things in recent years, sometimes in conjunction with quantitative signals, sometimes not.

If you’re posting to reddit, commenting on a blog or video, or publishing content yourself, you can be confident that the marketing departments of major credit card issuers are reading what you’re putting out there. Marketers report up to other departments on product usage trends and the voice of their customer. If the voice of their customer is yapping about a loophole its not supposed to have, a feature its not using as intended, or anything else of benefit beyond what is advertised, you can be certain those goodies will be killed by product leadership sooner or later.

Similarly, when chatting or on the phone with your friendly customer service rep, you should be aware that everything you say is being logged and analyzed in dashboards, meetings, and meetings about dashboards. Just as with marketing departments, surges in specific topics or questions stick out on the radar like a sore thumb. Badgering a bank employee about a key account feature that was retired will not magically turn that feature back on. Over a hundred of these calls will raise the question of why this feature is suddenly in demand, and prompt further investigation of customers who still have skin in the game.

Sharing away from the corporate eye does not guarantee privacy, either. Smaller online communities have their own share of participants who repost tips and plays without adequately gut-checking what it means for the survival of what they’re sharing. Some of these are from well-meaning churners excited to share knowledge with their peers and build community. Less forgivably, lurking influencers capitalize on community content by monetizing it for ad-supported blogs and paid courses. This latter demographic is a scourge and the reason you should know the agenda of your peers.

Finally, a common thread between all three audiences is the new variable of AI analysis. Every reddit post, chat or call log, or private community message is now subject to any number of agents ingesting, synthesizing, and summarizing its content ad infinitum. Despite bank technology having a reputation for being old and brittle, it is simple enough to batch export data and analyze it with another application. Many churners also use these tools, undisclosed, in private communities to manage the firehose of information coming at them on a daily basis. Even if you’ve forgotten what you once posted way up in the scrollback, or are past the 90 day window of your visible Slack content, don’t worry – AI remembers, and will always remember. The act of listening has now been delegated to a technology that never sleeps. Proceed with caution.

A footnote: “X has already been shared by popularwebsite, so it doesn’t matter if I share it again” is not a good excuse for indiscretion. Visibility on a play doesn’t come from one leak, but repeated signals indicating its heat and significance. Even if a play has been shared that cannot be unshared, abstaining from a repeat broadcast is good practice for extending its lifespan and diminishing its significance to those who would treat it indelicately – or those who have the power to see it killed.

So, what should we do when we don’t know who to trust? Build trust. Know who’s in the room by getting in the actual room. Get on calls, show up at meetups, and build churning relationships that turn into churning friendships. Gracefully retract and delete overshares when other churners let you know you’ve gone too far, and give a polite nudge when you see someone else spill too much (escalate as necessary). Despite only knowing each other by first names at best, the amount of trust in our hobby is uniquely special, and the only thing that keeps it together.

– $1,500 (or $2,000) sign-up bonus after $50,000 spend in six months – $295 annual fee – 2% cash back everywhere, (except 5% on AmEx Travel flights and hotels) – Cash back is not convertible to Membership Rewards

If you don’t see the heightened bonus, try VPNs, incognito browsers, mobile, letting the application timeout and reload, or summoning SideShowBob233. This card replaces the infamous Plum card, also a charge card.

Two Incomm gift card sites have fee-free gift cards:

Clearly this is because of the lack of oil flow through the Strait of Hormuz.

Delta has an award sale to its Asian destinations, but especially Taiwan and Hong Kong, running through today. Economy flights are 30,000-50,000 miles round trip, and in theory there are sale Delta One fares but they’re not exactly widely available so I wasn’t able to verify pricing.

Bilt added Wyndham as a 1:1 transfer partner. In a sea of bad ideas in travel hacking, transferring more than a de minimus number of Bilt points to Wyndham is a shark sized bad-idea.