EDITOR’S NOTE: If the math formula doesn’t render correctly in your reader, check the website at this link.

Introduction

In advantage play (gambling with an edge over the house), the Kelly Criterion or Kelly Formula gives a simple calculation for the best amount to bet to maximize earnings. We can draw an analog for resellers, whether it’s the buyer’s group kind or the gift card arbitrage kind.

The Propeller Head Part

The generalized Kelly formula, rewriting a bit to express terms familiar to resellers, is:

\%_{float} = \frac{(1-p_{loss})}{\%_{loss}} - \frac{p_{loss}}{\%_{gain}}Where:

- %float = The percentage of your budget to float

- ploss = The probability that you’re going to lose your profit

- %loss = The percentage you’ll lose if a loss happens

- %gain= The percentage you’ll gain if you don’t lose

A Simple and Specific Example

Let’s look at Pepper, which may or may not pull the rug out from under you at any point in the next year. With Pepper, you’re probably earning about 3.9% from your credit card (4x Membership Rewards, worth 4.4% cash back, times 90% due to Pepper’s convoluted redemption). Assuming your buy rate equals your sell rate after rewards are paid out (buy at 90%, sell at 90%), then we’ve got a simple calculation:

- ploss = 10% (pick your own number here, but let’s say there’s a 1 out of 10 chance of Pepper failure)

- %loss = 10% (worst case you lose all of the discount Pepper gives)

- %gain= 3.9% (the percentage you’ll gain if you don’t lose, in this case Membership Rewards)

Then run the numbers and get:

- %float = (1-0.10)/0.10 – 0.10/0.039 = 644% (when probability of loss = 10%)

What the hell, you might ask? Why is that number over 100%, and how do I invest that much? Well, the answer is either (1) you should float all of your bank roll to maximize profit because you’re much more likely to win than lose, or (2) you need 5.44 other players to help you.

Increasing the Chance of Failure

What if you think there’s a 30% chance of Pepper failure though? The calculation is again simple:

- %float = (1-0.30)/0.10 – 0.30/0.039 = -692% (when probability of loss = 30%)

What the double hell, you might ask? Why is that number over 100% and also negative? The formula is telling you that if you think Pepper’s got a 30% chance of failure in the next 30 days, you shouldn’t invest anything; “kill it with fire” says the formula.

Finding the Middle Ground

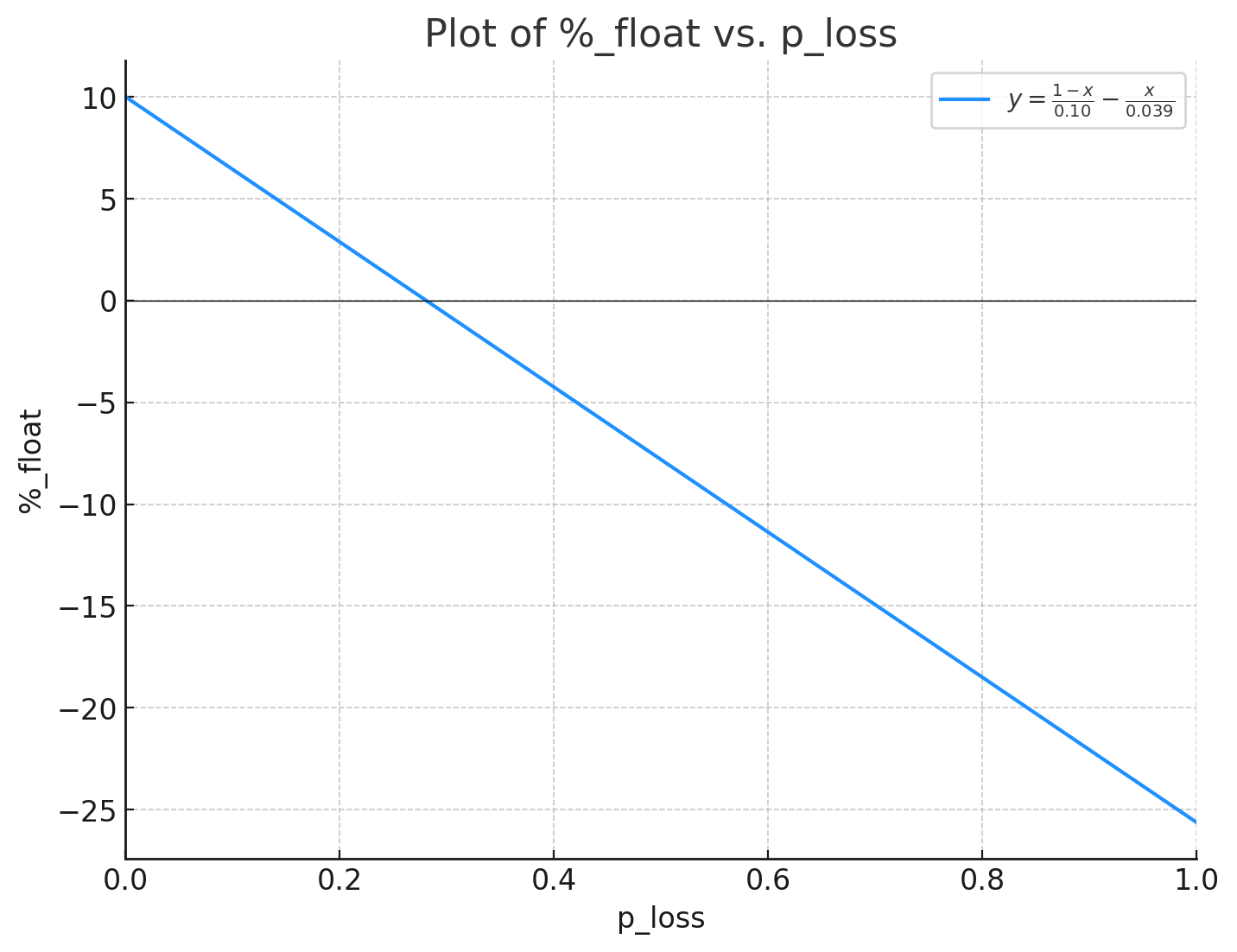

So, what’s the cut-off at which the formula switches from LFG to hells-to-the-no? I’ll spare you the algebra, but it’s easy to find by setting %float=0 and solving for ploss. Doing that gives:

- ploss (cutoff point) = 0.2806 = 28.06%

In other words, if you think Pepper is < 28% likely to fail before you can cash out your rewards, you’ll maximize your profits by playing the resell game. If you think Pepper is ≥ 28% likely to fail, stay away. (I generated a boring graph illustrating how float percentage varies with the probability of loss for turbo-nerds here).

{kind=link}

Conclusion

The Kelly criterion is surprisingly insensitive for churning problems, switching from above 100% (1.0) to below 0 very quickly. But, if you’re 3/4 certain that Pepper isn’t going to fail before your rewards are paid out, keep going.

Special thanks to John Reeder for poking me on the subject, and another special thanks to John for the idea for a follow-up piece on the subject: what if you know they’re gonna steal your money, but not when? Stay tuned, or, like yesterday, don’t; you do you.

Another helpful MEAB plot.