For the sake of illustration, let’s hypothesize that there’s a bank in america that supports payments through several different methods. Let’s also assume that the bank’s IT is bad and unpredictable. (That’s crazy, right?) Given that, it’s not to hard to imagine that different payment methods lead to different results; For example, the hypothetical bank refuses release credit lines on one payment method for up to 10 business days, but only sometimes. Using another payment method though, the same hypothetical bank releases its credit line within a day or two. Succinctly:

The credit line isn’t released for up to 10 business days using payment method A

The credit line is released 1-2 business days later using payment method B

Let’s add a further rub to this real-life hypothetical scenario: Assume payment method B might earn 50%-75% less than payment method A.

What’s the right thing to do in this situation? Remember the velocity of money. If you’ve got the spend to effectively use freed credit line quickly, earning half as much but being able to do it three to four times more often is still the higher earning play, because 50% * 4x > 100% * 1x.

Even though A pays more than B, B might earn more than A. Now, we just need to figure out C, I guess, or maybe just figure out what MEAB is driveling on about this time?

Have a nice weekend friends!

Let’s not even start with how to play with this beauty.

One of the hardest transitions between casual churning and becoming a heavy hitter is the switch from earning miles and points to earning cash back.

The transition should happen when you’ve earned all the miles and points you can spend cover your travel for the next 12-18 months, because:

Miles and points devalue by 30-50% in the span of years

The programs with the best redemptions change over time

Points don’t earn interest

The value of an unredeemed point is zero

Most of us don’t travel as much as we think we will (even if we travel a lot)

When you earn more points and miles than you can burn in a short time, the risk that excess points eventually become worth much less than when you earned them grows bigger than James’ Giant Peach from the famous historical documentary that I think is called “A kid finds a big fruit and someone wrote about it”.

Why do we fail to transition to cash back, even when we know analytically that it’s not the best option? The common answers I hear and that I’ve thought are:

Points and miles are fun, pennies aren’t

I’m motivated by travel, my job covers my cash needs

What if me and six of my closest friends need to fly Lufthansa F on last minute notice to Frankfurt and I don’t already have the miles banked, and my 800,000 Membership Rewards won’t post for another week?

They’re all valid reasons, but seeing them written can help prevent you from falling into the same trap. Trust me, you don’t want to be down 100,000 Hawaiian miles that expired a few years ago because you didn’t ever have an actual use for them and weren’t active in the program; $1,000 would have been a lot better. #askmehowiknow

The Pepper gift card platform, seemingly created as a conduit for moving money between venture capital bank accounts and gamers’ wallets, warrants discussion based on recent developments and crowd think.

Background

Moochoo, the company, the company behind Pepper, raised $23.05 million on December 21, 2023. Is it auspicious that they closed on a pagan holiday? Probably not, but it’s funny. Pepper’s go-to-market strategy started shortly thereafter with effectively unlimited 10% back (in Pepper coin currency) on new accounts for the first 15 days of the account’s existence, along with bonuses for the referrer. They appeared to want new users at all costs and turned a blind eye to gaming with zero due diligence on new accounts. (Have a new device? That’s a new person, obviously. It’s not possible to have more than one, duh. Just make those charts go up and to the right!)

Seven months later in July, Pepper pivoted its rewards scheme away from unlimited new account cash-back, almost certainly because at its then current burn rate, it wouldn’t survive long in the face of unlimited purchases of Walmart, Home Depot, Amazon, and other high value gift cards at ~90% of face value. Pepper replaced the new-user sign-up bonus with double base points on gift cards for the first 15 days, which wasn’t useful for bulk resale and caused volume to plummet. How do I know volume plummeted? Pepper order IDs are sequential, naturally.

The Now

Pepper took a few weeks, but they’ve settled into the new normal. Now, they release “Daily Boost” merchants once, twice, or three times a day. Boosted merchants earn much more than regular, like 12x on Amazon or 20x on Columbia Sportswear. Boosted merchants have a total capacity before the boost goes away, which sometimes happens in 30 minutes for popular brands and sometimes doesn’t happen at all.

The Warning Lights

There are a few recent developments that could be taken as warning lights:

Boosted merchant rewards payouts are now delayed by several weeks (is this related to cash-flow concerns?)

New accounts now require ID scans, but only as of a few weeks ago (why now, maybe because they’re trying to raise money and VCs want real user verification?)

Boosted merchant deals are getting better brands and higher payouts daily (why offer bigger than 10% discounts on high-volume bulk resale gift cards like Amazon, Walmart, and HomeDepot, which were probably burning Pepper’s cash reserves down like a dry Christmas tree on fire? Maybe to build temporary operating revenue?)

The capacity for boosted merchant deals seems to be increasing steadily (again, is this for cashflow reasons?)

Boosted merchant deals seem to be shifting to the brands that sell-out quickly from the brands that don’t (why push for more volume on cards you’re probably taking a loss on?)

To answer these questions, I think it’s time to build a simple quant-model for Pepper’s cash reserves.

The Pepper Doomsday Countdown

Let’s come up with a model for how much cash Pepper probably has left. The formula is really just $23.05 million, minus burned cash, plus earned profits. Let’s make some data-driven assumptions:

Monthly operating expenses, salaries, and benefits for 37 employees, assuming an average overall employee expense of $65,000 per year (this is likely a rather low estimate): 37 * $65,000 / 12 = $200,416 / month

Number of transactions through September 30, 2024 (order ID’s are sequential): 857,000

Average transaction size (bulk brands are usually between $750 and $1,500 in max size): $1,000

Monthly profit from regular discount gift card purchases for non-boosted accounts and users, assuming 3% profit: 3% * $500,000 = $15,000 / month

Per order losses on boosted transactions, assuming 3% loss: $1,000 * 3% = $30

Percentage of transactions that are boosted, in a new user sign-up bonus, or otherwise money losing: 80%

Now, let’s run the America-Loves-Math-o-tron-5000:

So, ~$23 million raised and ~$22 million in expenses by my simplistic toy model. You can play with the numbers and come up with your own conclusion, but you have to get pretty far below a 3% per transaction loss to make things look rosey for Pepper, or really far above $500,000 per month in profitable transactions.

Where does that leave me? I think Pepper is about 10% likely to die in the next 30 days, and maybe 50% likely to die by the end of 2024; unless of course they find another VC that wants to shoot money into a toilet. I’m still playing the Pepper game but only at a small level. If they fold and I lose my floated Pepper rewards, I’ll live without much regret.

Happy weekend I guess?

The result of the last round of Pepper’s VC money cannon.

One of the most click-baitey articles that travel bloggers write is: “What is [Airline] Status Worth? [Year] Edition”. I’m sick of seeing these articles, so I decided it was time to come up with the equivalent of the Drake equation, but for airline status because that’s apparently the best I can do with my life, and also it marks the first time that my astrophysics training has a real world application (except not really, see below).

Background

The Drake equation calculates the probability of finding alien life, provided that you’re willing to make a bunch of hand-wavey assumptions and then plug them into a formula. This, it turns out, is exactly what those “What is [Airline] Status Worth?” articles do too, except they calculate a dollar amount instead of probability.

So, in an attempt to make “the one airline status value formula to rule them all”, let’s, shall we say, go.

nphone = The number of times you’ll make a call to the airline

RH = The value of reduced hold time

nUI = The number of upgrade instruments you’ll earn and use

UI = The value of an upgrade instrument

BM = Bonus redeemable miles you’ll earn for holding status

nFPS = The number of free priority assigned seats you’ll get

FPS = The value of a free priority assigned seat

nup = The number of times you’ll be upgraded

FU = The value of a free upgrade (unironically abbreviated, I promise)

BT = The value of your elite brag tags, you know, like this

ANC = The value of ancillary benefits, like rental car status (that you probably already get from a credit card)

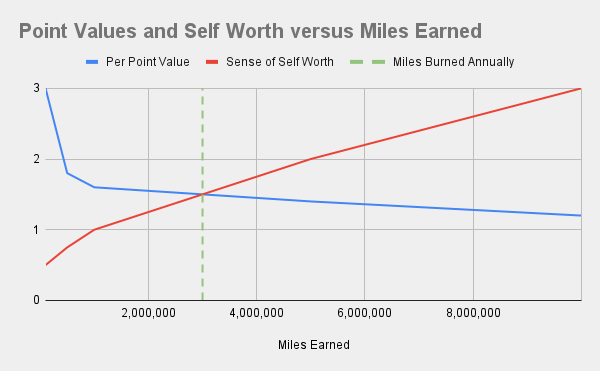

SSW = The value of your increased sense of self worth for holding elite status

So, just like the drake up equation, make up a bunch of numbers for what could happen and you’ll come up with the dollar value of your status. For example, I decided that my AA Executive Platinum Status is worth $3,430, but that’s mostly because of SSW. Remove that, and it’s probably worth $500.

Have a nice Thursday friends!

What’s the additional value of being served in a Delta branded cup on an AA flight? Science still doesn’t know.

Loops in churning are powerful because you can stack earnings as a dollar flows from a credit card, to a FinTech, to another, to yet another, and eventually (hopefully) back to your bank account to pay off your credit card. Instead of earning 3x on a single purchase, a loop might push the net earnings on that purchase well above 3x.

But if it’s good once, isn’t it better multiple times? Yes, but as you scale those loops across multiple cards, multiple players, and multiple charges in flight, tracking becomes a non-trivial load. Imagine keeping track of the following every day, knowing that any step in the chain might have a failure that needs manual intervention:

Buy a $499.51 sportsbook gift card

Load the sportsbook gift card into a FinTech account intermediary

Load the FinTech account’s funds into a sportsbook

Play through at least $499.51 in funds

Withdraw the $499.51±(profit/loss) into a FinTech’s rewards account

Use the FinTech’s platform to pay your credit card

Great! Now do that again 10 times per player, for 15 players, each with different initial gift card amounts for tracking, every day. Also, don’t forget to run your other plays that aren’t sportsbook related for the day too. Finally make sure you haven’t lost something along the way; I hope you’re good at Excel, Beancount, SQL, or something else to track it.

The Brick Wall

Some of the best churners I’ve met eventually take a few months or more off because tracking takes time, dealing with sludge when something goes wrong takes time, frozen accounts take time, and in net the mental load can push them to hit a brick wall and burnout.

Once you’ve burned out and stop manufactured spend, you earn exactly $0 per day, $0 per week, and since America Loves Math™, $0 per month too.

The Lesson

A loop can turn 3x earning into 6x, but too much looping and tracking can eventually turn into burnout which earns 0x. So, don’t forget simplicity and don’t be afraid to skip most of the steps in a loop to keep yourself sane when the world comes running at you.

Sometimes the path a dollar takes through a loop during advanced manufactured spend is staggering; As a semi-real world hypothetical, a manufactured spender might loop money around with a recipe like:

Run a charge with credit card on a fintech (earn on spend, perhaps pay a load fee)

Use a fintech virtual card to load another fintech (earn on spend, perhaps pay a load fee)

ACH out of the second fintech into a bank with a rewards debit (no earn or fee)

Pay the original credit card with your rewards debit (earn on spend, perhaps pay a payment fee)

Most of those steps have an earn component, and most have a fee component too. Calculating your total earn is really just a matter of adding all the earn and subtracting all the fees, and the goal is that the entire loop earns a nice spread.

Once you’ve developed a money loop like this, it’s easy to think of all spend fitting into the loop in someway.

But, and here’s the point of today’s article:

Sometimes skipping the middle steps earns just as much as the loop you’ve developed, or maybe earns slightly less but loops faster. Sometimes simplicity wins.

Have a nice weekend!

Simplicity can go too far, or sometimes not too far enough; which one is this churner’s house?

HawaiianMiles are easy to earn via American Express Membership Rewards

Alaska MileagePlan miles are valuable partially because Alaska is smaller than the big four major US airlines, and partially because again, they’re hard to earn. HawaiianMiles aren’t worth much relative to most major airline currencies, but if the merger completes then HawaiianMiles will balloon in value overnight.

The Play

Of course, gamers gonna game, and the opportunity to turn low value, easy to earn miles into more valuable miles is an obvious and attractive play. In fact, I’ll be running this play; I too like turning low value things into high value things just as much as the next churner.

The Scale

How big should you go? There are risks to going too big, namely:

Lots of people have a hard time actually using Alaska miles

On the first point, what’s the expectation value for a time to devaluation? I’d guess it falls between 18 months and 24 months based on past history. How bad is a devaluation? Usually, an average 30% increase in redemption cost is a reasonable upper limit.

The Answer

That brings a simple math formula to calculate how many miles to transfer: the number of miles I expect to redeem in the next 18 months, plus the number of miles to redeem in the following 18 months devalued by 30%, minus the number of miles I expect to earn in other ways.

The numbers for me, which are based completely on how many MileagePlan miles I earned and burned used over the last 18 months:

0-18 month range:

900,000 miles to burn

800,000 miles to earn

19-36 month range:

900,000 miles to burn * 130% for a devaluation

800,000 miles to earn

Running the math:

miles = (900,000 – 800,000 + 900,000 * 130% – 800,000 = 470,000 miles

So, 392,000 Membership Rewards transferred will cover me (probably) for the next 36 months. Very mindful, very demure, very cutesy. But, what about travel past 36 months from now, you ask? I guarantee my situation, the US airline situation, airline transfer partners, airline alliances, and my travel needs will be different in 36 months, and speculation beyond that timeframe is at best a guessing game, especially since an unredeemed point is worth zero.

A balancing act that we frequently face in manufactured spend and churning is knowing how hard to hit a deal. If you push it too hard, you may kill it in days. If you don’t hit it hard enough, you’re leaving money on the table – potentially a lot.

What’s the magic behind how hard you should hit a deal and when you should back off? In my mind it comes back to two fundamental questions:

Who’s paying for your earnings?

What metrics, compliance, and regulations are important to them?

If you can answer those two questions then you’ve got a guide for how much abuse a deal will tolerate. If, for example, you’re dealing with a small, local casino’s loyalty program that’s relentlessly focused on bringing in gamblers, you can bet that they’ll know pretty quickly if they start paying out a ton of rewards due to your shenanigans. So, I’d treat such a thing as a short, surgical strike and try and run the deal low and slow over months or years.

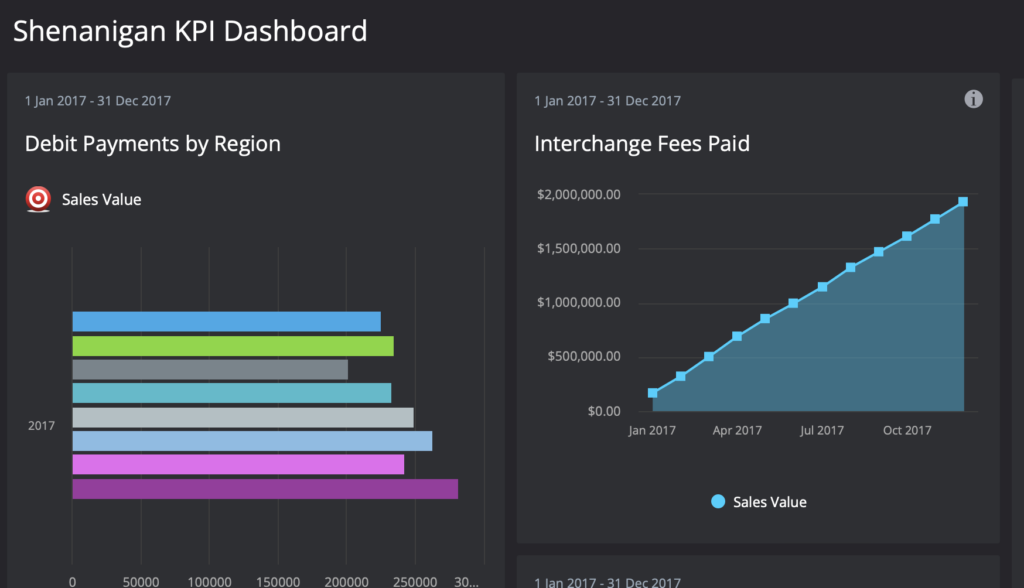

On the other hand, if you’re dealing with a dinosaur bank that has disconnected legacy systems and trillions of dollars in assets, your debit card funding would probably have to get well into seven or eight figures before it showed up as a blip on anyone’s KPI dashboard, and on top of that they’d have to be curious enough when they see it to dig in and figure out what’s going on. So, this one is a probably a pedal to the metal play, understanding that time and not volume will probably make the deal die.

So, an unsolicited suggestion: When you encounter a new deal, think about who is paying for it and what their regulations are as a guidepost.